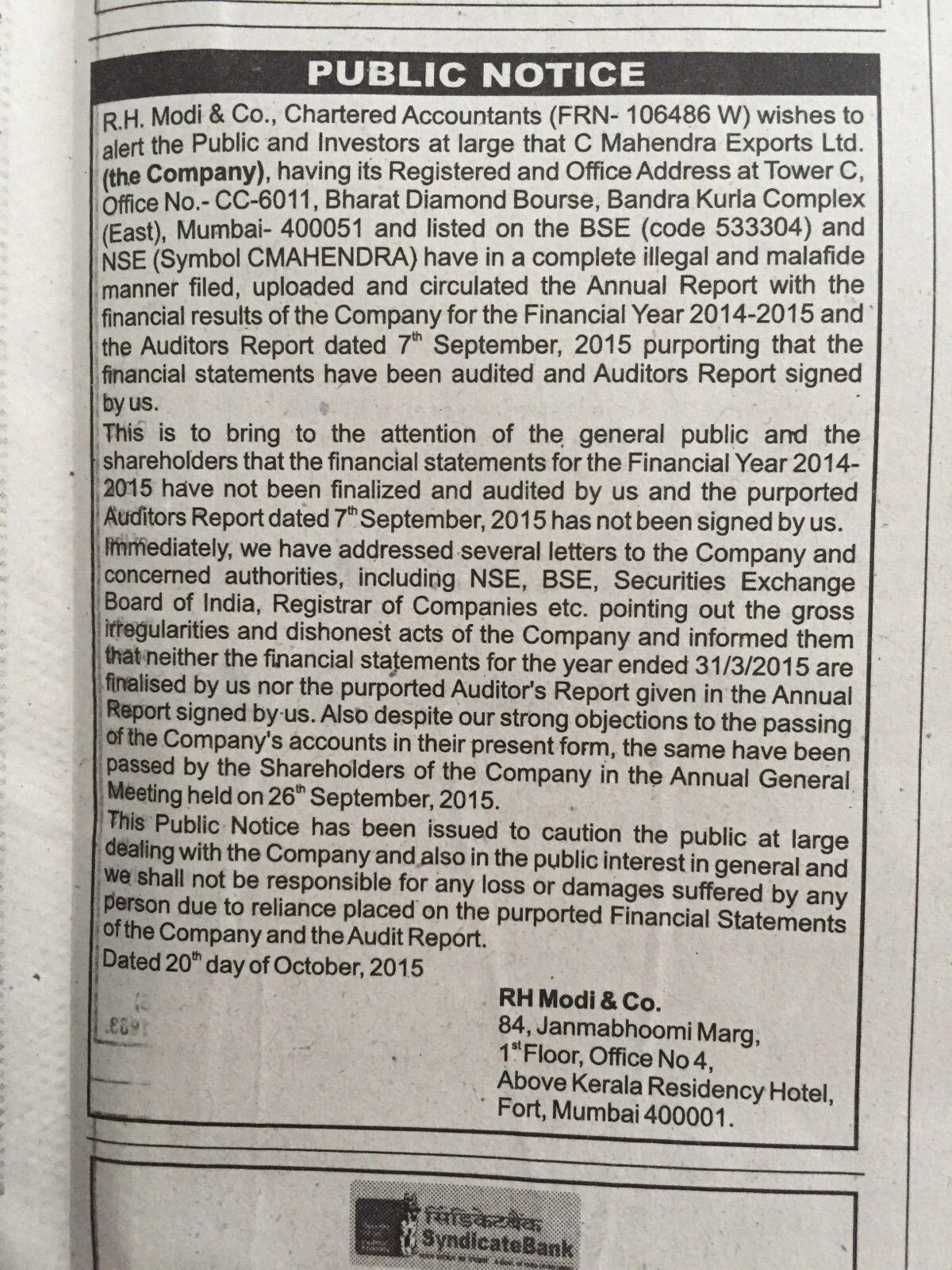

Indian corporate world was shocked and corporate governance became a question when on 20th October 2014, M/s. R. H. Modi & Co., Chartered

Public Notice by Auditors

Accountants, auditor of C. Mahendra Exports Limited published a public notice in newspaper. It was alleged that the company “in a complete illegal and malafide manner filed, uploaded and circulated the Annual Report with the financial results of the company for financial year 2014 – 15 and the auditor report dated 7th September 2015 purported that the financial statements have been audited and Auditors Report signed by us (M/s. R. H. Modi & Co., Chartered Accountants).

The auditor in this public notice claimed that these financial statements have not been finalised and audited by them. The auditor claimed that despite their strong objection to the passing of company’s account in their present form, the same have been passed by the shareholders of the company in annual general meeting held on 26th September 2015.

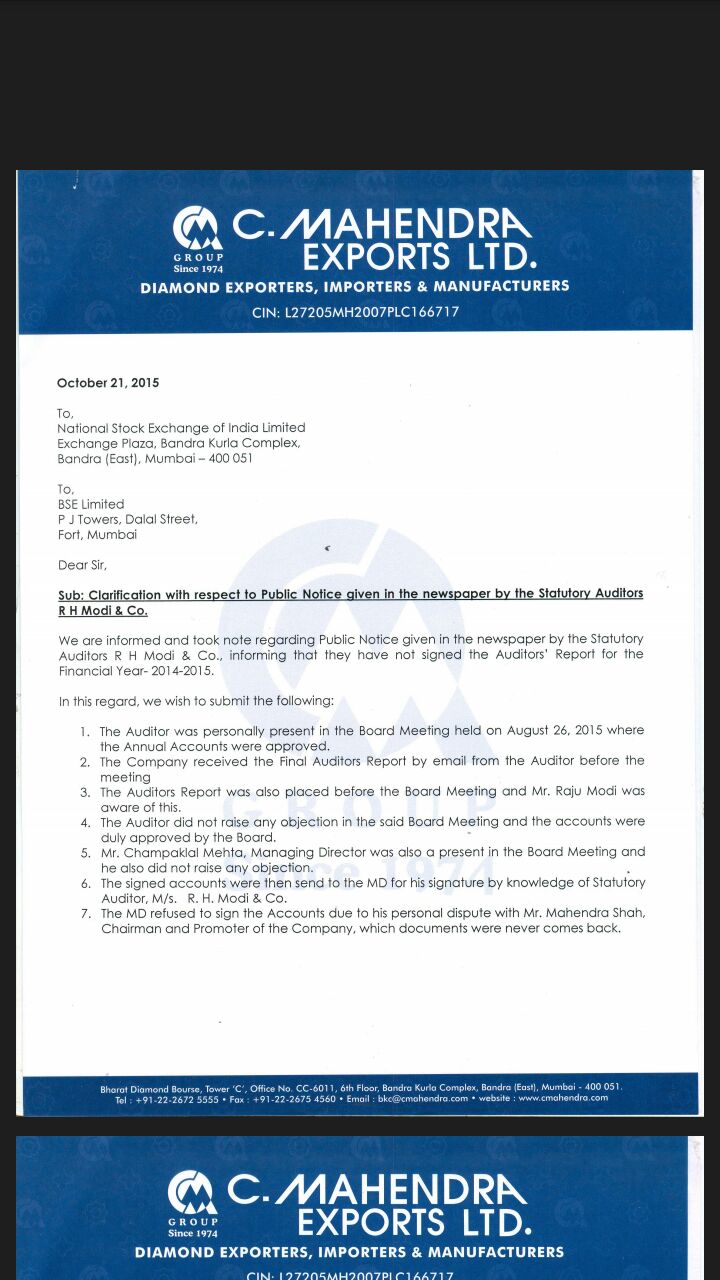

The company filed its clarification before stock exchanges, which is available in site of Bombay Stock Exchange here and site of National Stock Exchange here. The company not only stated facts from their side but also raised several questions on point of law.

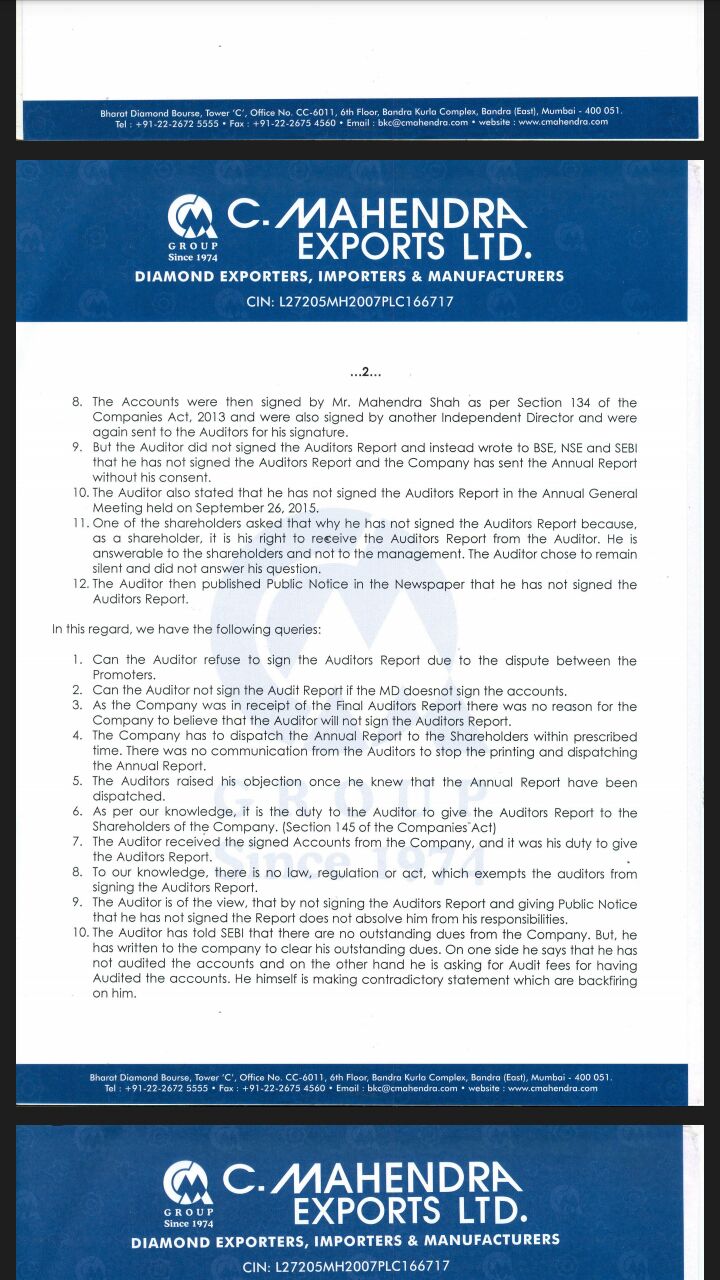

According to facts mentioned by the company, Managing Director and Statutory Auditors did not sign the financial statements and Auditors Report. The company presented following interesting queries:

- Can the auditor refuse to sign the auditor’s report due to dispute between the promoters?

- Can the Auditor not sign the Audit Report if the MD does not sign the accounts?

Fully clarification written by the company is worth academic reading.

This blog does not want to discuss on the matter which may soon go to inquiry by relevant professional bodies and regulators. However, development on this matter may be of academic interests.

Reply by Company P.1

Reply by Company P.2

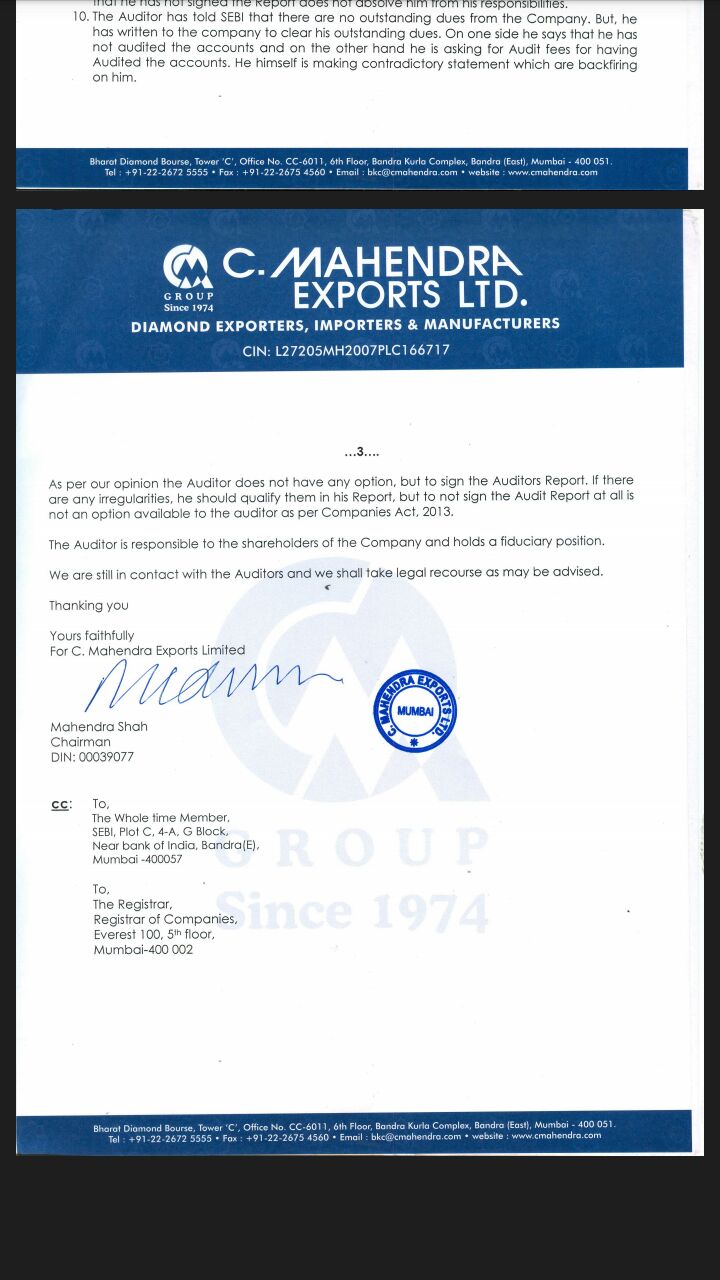

Reply by Company P.3