The recent consultation paper issued by the National Financial Reporting Authority (NFRA) generated lot of discussion in media, social media and professional circle. This consultation paper is first serious attempt from regulators to discuss a critical issue of compliance. I have made suggestion to remove requirement of compulsory audit to the Company Law Committee constituted by the Ministry of Corporate Affairs in year 2018, though not considered by the committee. I am sharing my views on this well studied consultation paper in public before submitting it to the NFRA.

Quality Concerns

The quality of statutory audit, cost audit and secretarial audit are not satisfactory because of a valid reason for which blame should be shared by the legislature. Auditors are not investigation agencies but just a watchdog who could not bark just report to Chaukidar aka Regulator. Auditors have to relied on documents, if made available or for rest on management representation letters. He cannot ascertain the truth in the representation so made, even if a suggestive draft is made by him. No such representation is made on an oath under law. The auditor have to assume it as true. Except a few cases of Government audits or regulatory audits, all auditors are appointed and importantly paid by the management of the company – the auditee not by the shareholder or any other stakeholders. None of our paymaster want any thing which may trouble the management, our paymaster.

We have number of tax audits but requirement of assessment, re-assessments and more seriously tax raids, (whatsoever fancy names government call it) are there. Should not the tax computed by the management and confirmed by tax auditor be final. If the government think it is not, these audits are Ponzi scheme of employment generation for benefit of we – the professionals.

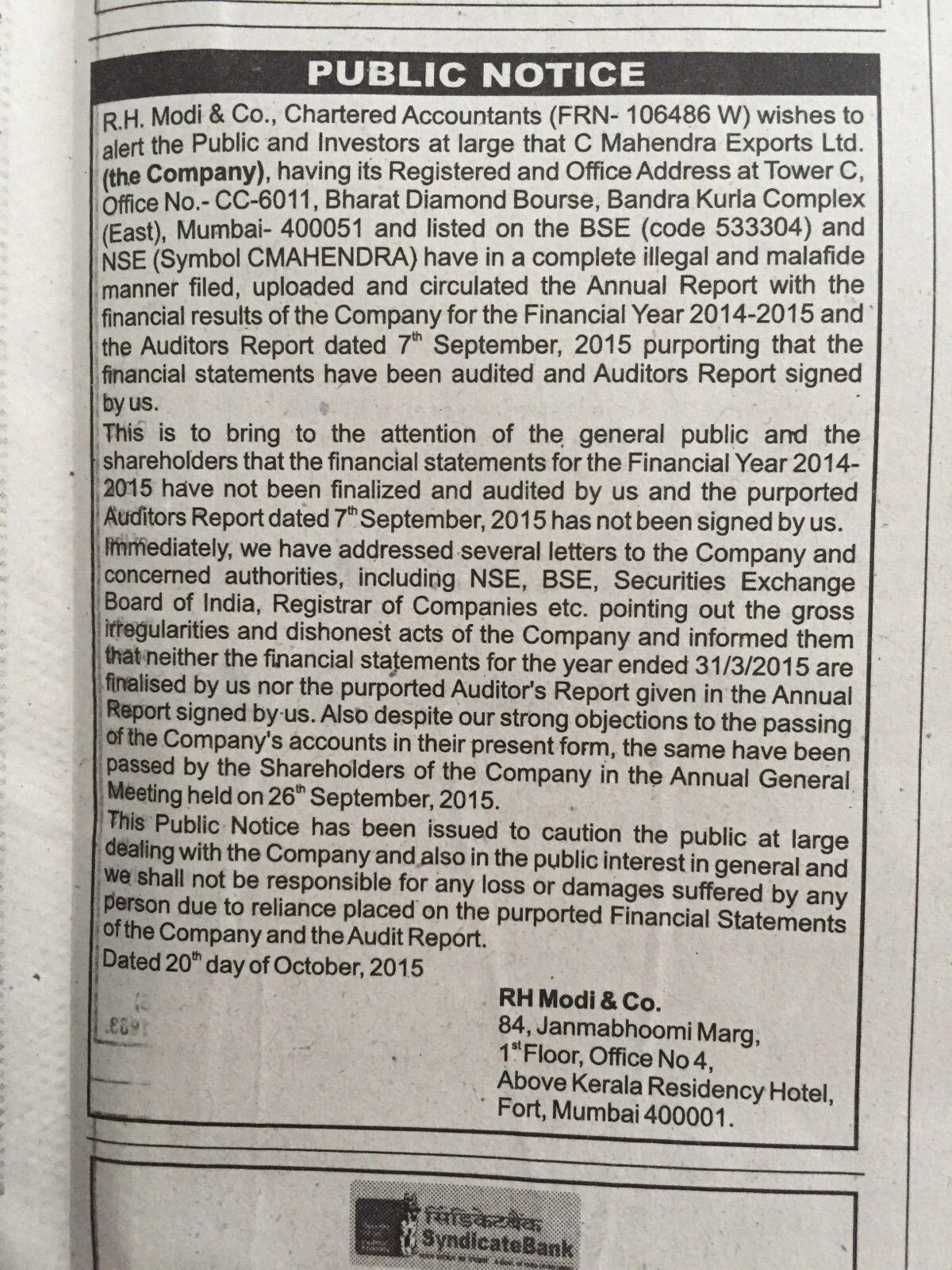

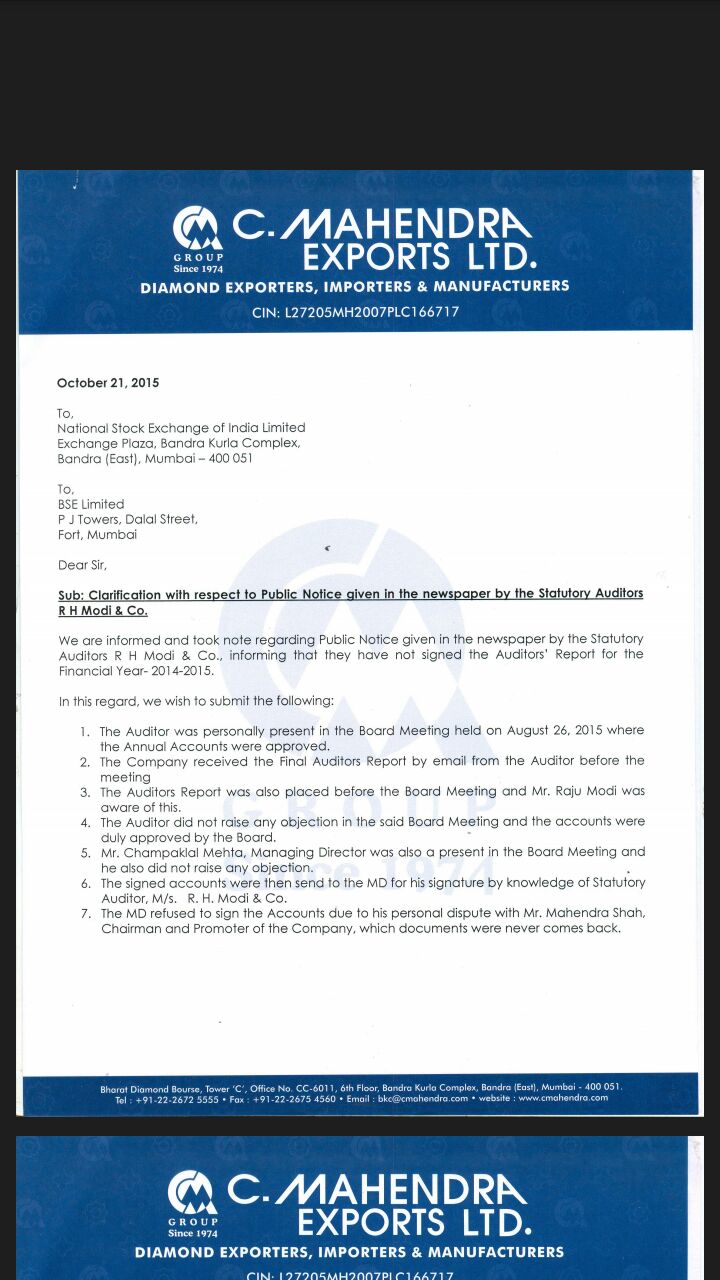

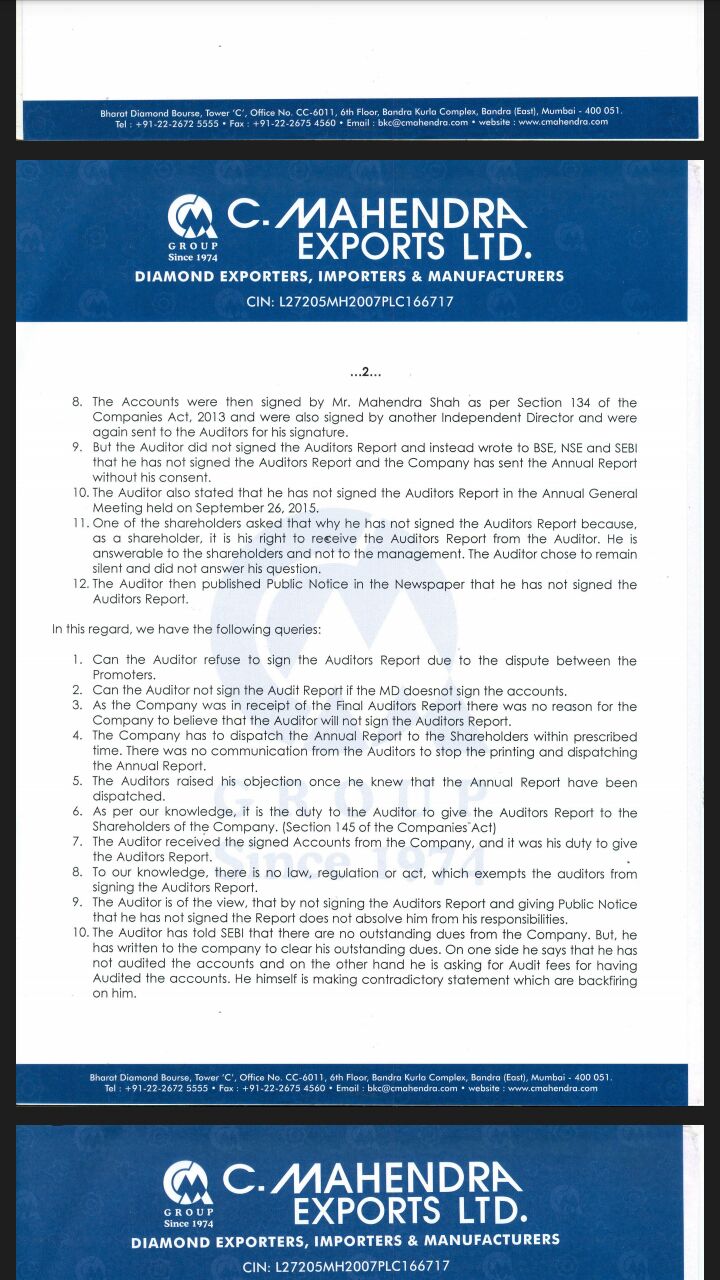

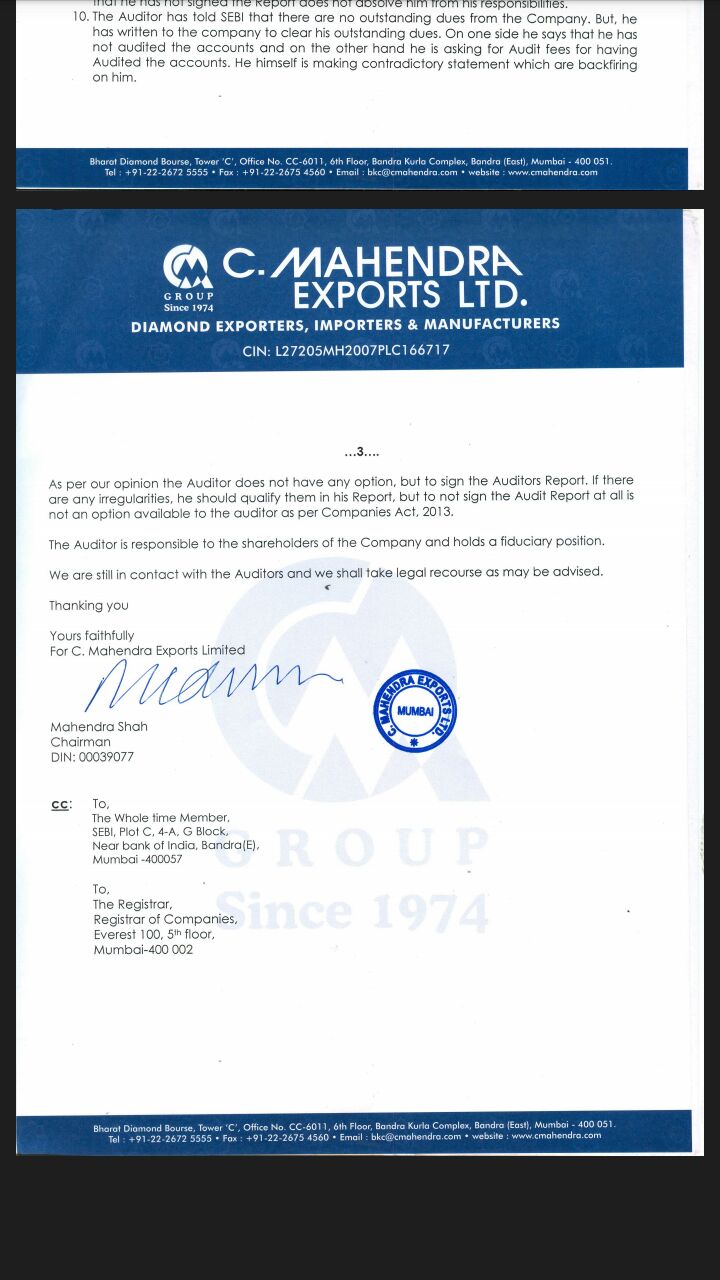

Same way we have Satyam, Sahara, Sharada, DHFL, Srei and a long list of corporate fraud. Either auditors were co-accused or helpless. In year 2015, an auditing firm issued a public notice that the client is fraud. That was an interesting case showing helplessness of auditors. All major non-performing assets of Bank are of well audited companies. Almost all cases of non-cooperation under the Insolvency and Bankruptcy Code auditors are one of the helpless respondents. Even Forensic and Transaction Audit do not have satisfactory result. But if audit is there, why should we need so many Forensic and Transaction Audit?

Few years earlier when a reputable law firm was under scanner of law enforcement agency in a scam, private chats were full to claim professionals – Corporate Law firms, Chartered Accountants and Company Secretaries as gurus of fraud not as whistle blower. What MCA data on fraud reporting by these professionals say in relation to corporate fraud in limelight? There is no real power and motivation but pay-cuts, resignations, removal and punishment.

In corporate history the most cited reason of the resignation as position of auditor is personal reason (?), Health (??) old age (?), paucity of time (??) when without any such reason we continue with audit of other companies.

I am happy to note in most reportable frauds we have globally reputable auditing and legal firms to name (and shame?) who have most exhaustive check lists to marks ticks in mechanical manner.

Compliance Concerns

Except a few, promoters have no inbuild intention to comply the law in spirit. Most of the time they do not bother on annual filing of accounts and even taxation considering it as useless cost unless there is a fine, penalty or imprisonment is waiting. Promoters leaves everything to ‘manage’ by the professionals. Only 52.48% companies filed annual account and annual return with MCA for year 2018-19 till the consultation papers while the last date was 30 September 2019. Earlier when the Ministry strike off name of many such companies defaulting in filing of annual accounts and annual returns, the most used ground to seek restoration was lack of professional advice. If you have no idea of the route of business in corporate, why are you on the corporate highway? Promoters need to be responsible from day one. Contrary to the legislative intention, Audit provide them window to shift responsibility and blame.

Compliance Cost

This is interest data shared in the consultation paper: 30.26% companies paid no fees to the auditors, 6.79% companies paid less than Rs. 5,000/-. No professional can devote more than 5 hours on these audit assignments in reality. What assurance these accounts and audit provide to stakeholders? No, I am not raising question on all these companies as professionals give huge discounts to new companies, companies with no turnover or facing troubled time. A good number of these assignment may be attached with a well-paying group company or promoter. In a good number of these companies the auditor himself or their related entity write accounts. However, question remain of the real value of the audit in these companies.

In these cases, the audit is not the actual assignment. The actual assignment is account writing. The audit assignment just ensure that the account writing will not go to a non – professional accounting graduate and may improve the quality of accounts slightly.

Baseline of NFRA Consultation

“A majority of these MSMCs is essentially family-owned enterprises formed as companies for the sake of limited liability, or to get bank loans, bus route permits, mining licences, and the like. They are effectively glorified proprietorships or partnerships. There is no public interest in foisting external audit on them. In any event, it is clear that such audit as is being carried out cannot boast of any quality at all.”

I have no disagreement on this observation except limited liability concept. Limited liabilities of a promoter end in India as soon as a company seek loan. Personal Guarantees of promoters effectively make small companies unlimited liability firm in real sense. (Discussed this aspect earlier here). These promoters do not attract with the limited liability concept. They choose a reputation called director or managing director, which comes with a company. If they have money and big family, they will not choose a private company but public company as in popular terms directorship of limited company bring more reputation than directorship of private limited companies. Same time various rules related loan, license, authorizations, permits and like favor companies than partnerships and proprietor firms. You can choose a good and unique name unlike partnership and proprietor concern which have no mechanism to ensure unique name.

I agree there is no benefit of audit in a family-owned company without any external liabilities. To my understanding all companies with small shareholding should have self-certification from shareholder – directors about the fair and correct accounts. We have such practice in case of limited liabilities firms. They may otherwise made aware not to make such certificate unless they are sure or have counter certificate from a professional.

However, in the audit may be conducted without requirement of filing audit report to the Government, where:

- article require audits;

- a shareholding or investment agreement require audit;

- there is a contractual requirement of audit;

- the board of director opt for audit;

- Shareholders with a simple majority opted for audit of one or more year;

In following cases, there audit report should be filed with the Government:

- Any enforcement agency requested an audit for ono or more year;

- One or more scheduled bank require audit with filing of such requisition to MCA by such bank. In such case, the auditor appointed in first requisition shall conduct audit. In case of any subsequent request, report of auditor appointed in first request be made available to all banks having exposure.

- Where there is a repayment default for three continuous months or four months in a financial year, an audit including a forensic and transaction audit be conducted with prior intimation by banks to RBI and MCA.

- The company made an erosion of net worth of more than 10% after 3 years from incorporation, on application by shareholders with more than 1% shares, the Registrar of Companies may direct companies to have an audit.

- Where company fail to file its self-declaration accounts and annual return for more than two financial years.

Whether or not my suggestion accepted, I will strongly suggest no statutory audit in first five years for a small company.

NFRA requests views/comments

| NFRA Question | My Draft Reply |

| Do you think that Micro, Small and Medium Companies (MSMCs) depending upon some criteria and threshold should be exempted from the mandatory statutory audit under Companies Act, 2013? If not, why not and if yes, what would be the criteria and thresholds for exemption? | Yes. All MSMCs which are private companies with less than 10 members having voting powers should be exempted from mandatory statutory Audit. All MSMCs which are wholly owned subsidiaries may also be exempted. In case of all contractual requirement of audit, filing should not be required. In case of certain well enumerated defaults or requisitions, the Registrar of Companies may order audit for one or more years being year not earlier than 3 years from the date of such order. Such audit report may be required to be filed with the Registrar and be a public document. |

| Do you think there is a requirement for a separate set of auditing standards for MSMCs as it exists for accounting standards? If no, why not and if yes, what should be the basis for the same? | I do not think so. All companies should have accounting and audit on same pattern, where require to have audit. This will help companies to follow same set of internal and external audit upon growth. This will also help investors, present and future |

| The cost of conducting an audit as per the prescribed standards is an important input for the responses to Questions 1 and 2. Do you agree with the approach for estimating standard cost of audit computed by NFRA? If not, which areas/ assumptions need changes? | The cost of conducting an audit should not be prescribed and should be leaved to the market forces. However, where it is unreasonable low or high, the auditor should explain. |

| Do you think the current exemption thresholds for CARO, ICFR and statutory audit applicability need to be standardised and made uniform? If no, why not and if yes, what would be the criteria and thresholds? | Other than exemption to MSMCs, no change is required as of now. All companies where CARO, ICFR and Statutory Audit is not applicable, there should be a corresponding self-declaration to file with the Registrar signed on behalf of the Board and be placed in the General Meeting for adoption. |