The law stated in this post was valid from 14th June 2018 till 7th February 2019. The post on the law applicable from 8th February 2019 is posted here.

Section 90 of the Companies Act 2013 substituted by a new set of law. It is a drastic change to understand and need urgent attention for all companies. Amended Section 90 and rules made thereunder has been notified with effect from 13th June 2018 and 14th June 2018. The significant deadline is on 12th September 2018 with a lot of working and follow up required, coincide with all Annual General Meeting, Annual filing and tax returns. In this post, we will discuss what constitutes Significant Beneficial Ownership.

Note: Earlier Section 90 {Invesigation of Beneficial Ownership} as applicable form 1st April 2014 to 13 June 2018 was discussed here.

Beneficial Interest

Beneficial Interest under the company law commonly used to mean as holding share as nominee (read trustee) of another person usually a body corporate, mostly to satisfy requirement of minimum shareholders.

Newly, inserted sub – section (10) of section 89 define beneficial interests for the purposed of Sections 89 and 90.

Beneficial interest in a share includes, directly or indirectly, through any contract, arrangement or otherwise, the right or entitlement of a person alone or together with any other person to—

(i) exercise or cause to be exercised any or all of the rights attached to such share; or

(ii) receive or participate in any dividend or other distribution in respect of such share.”.

First clause of the definition gives it a wider meaning. Such right may be any right which may be attached with such shares – security interest, dividend, bonus, trust, bailment, pledge, right related to sale or purchase, pre-emption, succession, actionable claim and so on.

Significant Beneficial Owner

Subsection (1) of section 90 define significant beneficial owner. Every individual who holds beneficial interests, of not less than twenty-five per cent or such other percentage as may be prescribed (reduced to ten percent by rules), in shares of a company or the right to exercise, or the actual exercising of significant influence or control as defined in clause (27) of section 2, over the company is Significant Beneficial Owner.

Such significant beneficial ownership of an individual may be by acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India.

Rule 2(1)(e) of the Companies (Significant Beneficial Owners) Rules 2018 further explain that “significant beneficial owner” means an individual referred to in sub-section (1) of section 90 (holding ultimate beneficial interest of not less than ten per cent) read with sub-section (10) of section 89, but whose name is not entered in the register of members of a company as the holder of such shares.

The term ‘significant beneficial ownership’ shall be construed accordingly.

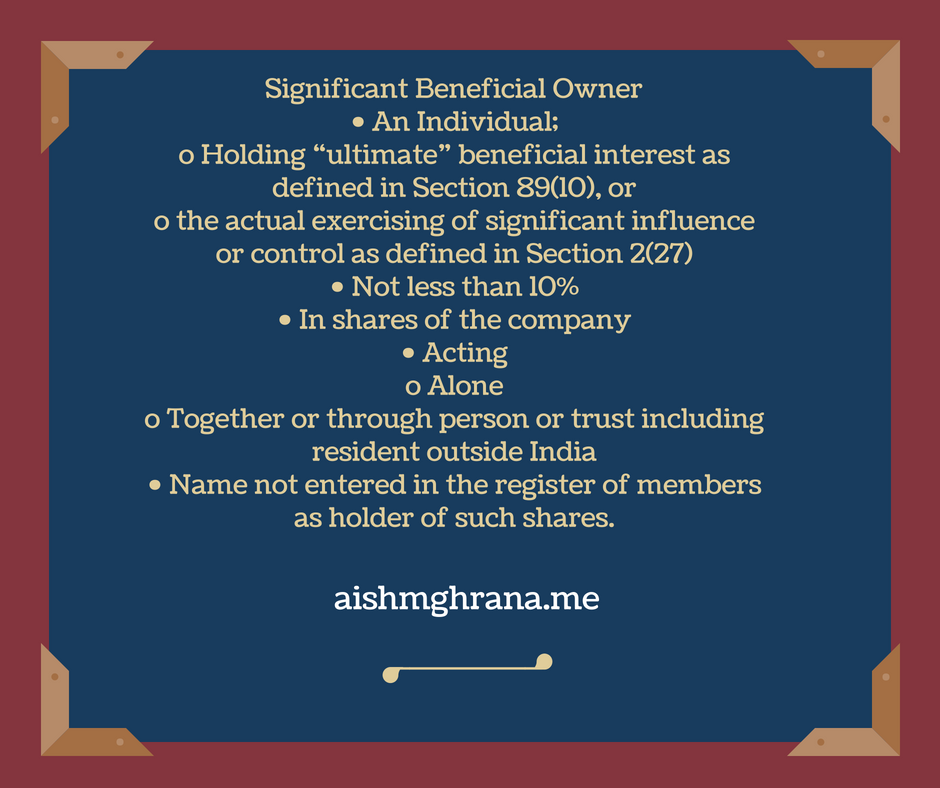

Significant Beneficial Owner – pointed definition

- An Individual;

- Holding “ultimate” beneficial interest as defined in Section 89(10), or

- the actual exercising of significant influence or control as defined in Section 2(27)

- Not less than 10%

- In shares of the company

- Acting

- Alone

- Together or through person or trust including resident outside India

- Name not entered in the register of member as holder of such shares.

Shares for Significant Beneficial Ownership

Explanation II of Rule 2(1)(e) say instruments in the form of global depository receipts, compulsorily convertible preference shares or compulsorily convertible debentures shall be treated as ‘shares’ for the purpose of this clause.

An instrument (GDR, PS, or Debentures) compulsorily convertible to equity shall be treated shares. Any other instrument and optionally convertible instruments are not shares under this definition.

Determination of significant beneficial interests

The question of beneficial interest and significant beneficial interest shareholding of an individual may be settled easily. Tough question arises when shares, beneficial interest or significant beneficial interests is hold by a body corporate, trust or partnership and more so, if held by in layers. Explanation I of Rule 2(1)(e) helps:

Beneficial interest through a company

Where the member is a company, the significant beneficial owner is the natural person, who, whether acting alone or together with other natural persons, or through one or more other persons or trusts, holds not less than ten per cent share capital of the company or who exercises significant influence or control in the company through other means.

Beneficial interest through a partnership

Where the member is a partnership firm, the significant beneficial owner is the natural person, who, whether acting alone or together with other natural persons, or through one or more other persons or trusts, holds not less than ten per cent of capital or has entitlement of not less than ten per cent of profits of the partnership.

Beneficial interest through a company

Where no natural person is identified under (i) or (ii), the significant beneficial owner is the relevant natural person who holds the position of senior managing official.

Beneficial interest through a Trust

Where the member is a trust (through trustee), the identification of beneficial owner(s) shall include identification of the author of the trust, the trustee, the beneficiaries with not less than ten per cent interest in the trust and any other natural person exercising ultimate effective control over the trust through a chain of control or ownership.

Beneficial interest through a Body Corporate

Where the member is a company, there is no process of determination is suggested in these explanation. However, it may be construed in suitable manner.

Declaration by Significant Beneficial Owner

Such significant beneficial owner shall make a declaration to the company, specifying the nature of his interest and other particulars, in such manner and within such period of acquisition of the beneficial interest or rights and any change thereof, as may be prescribed.

We will discuss the declaration and other aspects of this law in other posts here.

Exemption from declaration

Central Government may prescribe a class or classes of persons who shall not be required to make declaration under this sub-section.

First thing to note, Notification GSR 463(E) dated 5th June 2015 exempts government companies from applicability of section 90. However in case of public – private partnerships I suggest a conditional exemption only.

According to Rule 8 of these Rules, these Rules are not made applicable to the holding of shares of companies/bodies corporate, in case of pooled investment vehicles/investment funds regulated under SEBI Act:

- Mutual Funds,

- Alterative Investment Funds (AIFs),

- Real Estate Investment Trusts(REITs), and

- Infrastructure Investment Trusts (InvITs).

Significant Beneficial Owner

Pingback: Declaration by Significant Beneficial Owner | AishMGhrana

Pingback: Seeking information of Significant Beneficial Ownership | AishMGhrana

Pingback: SIGNIFICANT BENEFICIAL OWNER | AishMGhrana

Pingback: Declaration by Significant Beneficial Owner | AishMGhrana

Pingback: THE FORM BEN – 2 | AishMGhrana

Pingback: THE FORM BEN – 2 | AishMGhrana